Hello friends,

We hope this letter finds you well. Over the past few years, we have witnessed a steep increase in the prices of precious metals such as gold and silver. We have fielded some inquiries so we thought it would be of interest to you if we organized our thoughts on this topic in a letter.

What’s going on in the market for silver and gold?

In 2025, gold and silver had their largest annual gains since 1979. In 2026, gold and silver prices experienced significant volatility. According to the Globe and Mail gold plunged 10% on Friday, January 30, 2026 – its biggest decline in more than 40 years”[1].

A recent Barron’s article sums up the recent price swings:

“What a ride it has been for silver. Prices were up almost 50% in 2026, to $100 an ounce, through Thursday’s close, and had tripled over the past year, with the metal trading as high as $120 an ounce this past week. Then it all fell apart. This past week was one of the most volatile periods ever, capped by a 31% drop in silver to $85 an ounce on Friday, the largest absolute drop in history and the biggest percentage decline since the Hunt Brothers tried—and failed—to corner the market in 1980[2]”.

What has been driving recent gains in gold and silver?

There are many possible factors cited including inflation fears, global geopolitical instability, a lack of faith in currencies, U.S. debt and fiscal concerns, AI infrastructure demand, etc.

A recent Globe and Mail article explained the popular sentiments: “[Gold] has also long been considered the world’s safest asset, attracting buyers seeking a store of value, a hedge against inflation, a haven during periods of volatility, portfolio diversification or a mix of all four[3].”

Silver, one of the best conductors of electricity, has also benefitted from an increase in industrial demand, which typically accounts for around 60% of total silver consumption[4]. Silver may also benefit to some extent from the massive buildout of AI infrastructure; however, cheaper substitutes may buffer this demand[5].

Lastly, central banks around the world have been buying more gold and moving away from the U.S. dollar, as reported by the Globe and Mail: “This multi-year diversification away from the greenback has been driven, in part, by growing unease about U.S. foreign policy, including the aggressive use of sanctions, as well as the country’s unsustainable fiscal trajectory[6].”

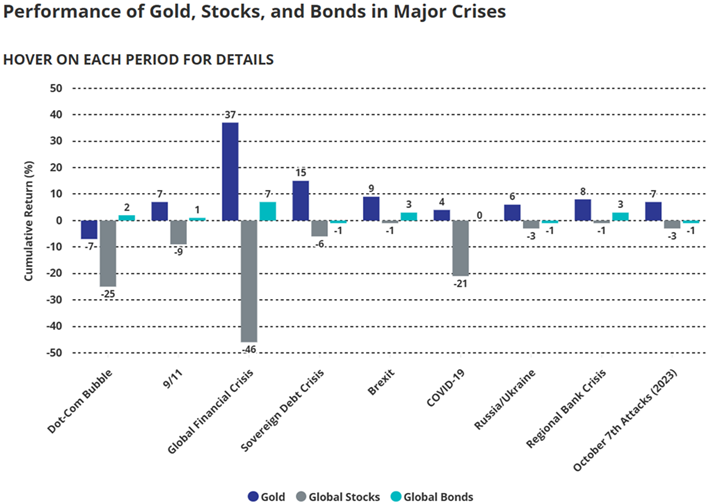

Gold has at times outperformed stocks and bonds.

Investment in gold and silver has, at times, outperformed stock indices such as the S&P500. Warren Buffett ceded this point in a 2011 appearance on CNBC’s “Squawk Box.”:

“Basically, gold is a way of going long on fear and it’s been a pretty good way of going long on fear from time to time, but you really have to hope people become more afraid in a year or two years than they are now. If people become more afraid, you make money, and if they become less afraid, you lose money, because the gold itself doesn’t produce anything[7].”

It is true, generally that gold has held up during bear markets / crises in stocks as can be seen in the following chart[8].

However, the market for gold and silver has been characterized by periodic cycles…. often devastating to those late to the party.

Many of you will know that we have experienced several cycles in the prices of gold and silver over the past several decades. These cycles have been characterized by periodic bubble episodes, followed by sharp declines and long periods of stasis.

According to Google’s Gemini:

“Over the past 100 years, gold and silver have experienced several significant, distinct, and sometimes overlapping bubble cycles, typically driven by macroeconomic crises, high inflation, and, in the case of silver, market manipulation. While gold is generally seen as a long-term store of value, both metals have historically reached speculative peaks followed by severe corrections (emphasis, ours)”.

Major Gold & Silver Bubbles (1926–2026)

The 1979–1980 Hunt Brothers Silver Bubble: This is considered one of the most famous commodity bubbles in history. Silver prices surged from around $6 an ounce in January 1979 to nearly $50 in January 1980 (an over 800% increase), driven by the Hunt brothers attempting to corner the market. It ended in a “Silver Thursday” crash when exchange rules changed, causing a 25% drop in one day and pushing silver to $10 by March 1980.

The 1980 Gold Peak: Gold peaked around $711/oz on January 21, 1980, as a result of the “Great Inflation” and geopolitical tensions, before falling by over 57% to $304/oz by June 1982.

The 2008–2011 Post-Crisis Rally: Following the 2008 financial crash, both metals saw massive, driven by safe-haven buying. Silver peaked near $50 again in April 2011 before crashing, and gold hit a record high (at the time) of over $1,900/oz in 2011, followed by a multi-year bear market.

The 2020s Pandemic & Inflation Bubble: Driven by pandemic-era money printing, inflation, and geopolitical risk, gold crossed $2,000/oz for the first time, with sustained highs between 2020–2025.

2025–2026 Gold/Silver Surge:

- In 2025, gold surged more than 60%, surpassing $4,000 per ounce for the first time in October. By early 2026, it peaked as high as $5,500 per ounce before undergoing volatile corrections.

- Silver significantly outperformed gold, skyrocketing 147% in 2025. In January 2026, silver breached the psychologically significant $100 mark, peaking near $121 per ounce.

What is the long-term performance of gold & silver compared to stocks?

So, gold and silver have done well during certain periods, but what is the long run performance relative to alternatives such as stocks (S&P 500)? To answer that question, we provide commentary from NYU professor Aswath Damodaran, who compared stocks to gold over the 40-year period of 1984-2024 (granted, this period excludes the 2025-26 rally). Damodaran, considered by many to be the “Dean of Valuation”, had this to say in a November 2025 blog post:

“Looking at the last forty years of returns on different investment classes, you can see why making an argument for holding gold as your core investment is so difficult to justify.

Gold, with its annual compounded return of 5.35% between 1984 and 2024, would have significantly underperformed an investment in US stocks, that earned a compounded return of 11.38%, a difference that translates into a significant shortfall in ending portfolio value for gold investors; investing in US stocks in 1984 would have generated almost ten times as high an ending value in 2024, as investing an equivalent amount in gold in 1984[9]”. See chart below:

{kind=link}

So, stocks are a superior investment owing to the compounding nature of earnings. Companies produce earnings, which can grow exponentially like the ancient fable of a mathematically challenged King, a grain of wheat and a chessboard (abridged version: a grain of wheat doubled 64 times yields 18 quintillion grains, an amount far exceeding modern global wheat production and enough to cover the entire Earth).

Is Gold a Safe Haven?

Historically, gold has been as a safe-haven or a form of insurance in times of crises but the perception of gold as a “safe” investment may be illusory. In fact, the price can be quite volatile, particularly during bubble episodes.

Case in point: Someone who bought bullion at its 1980 peak would have had to wait 25 years to get back to even – it lost 82 per cent of its value in real terms over the following two decades[10]. Someone who bought gold at its 2011 peak would have had to wait nine years to be back to where they started[11].

A recent Financial Times article sums it up nicely:

There may be a meaningful way to describe gold as insurance; it cannot meaningfully be described as a low-risk asset[12].

The Debasement Theory

A popular narrative today is that gold and silver may be a possible hedge against “debasement”. The debasement argument goes that currencies like the U.S. dollar will continue to lose purchasing power due to high levels of government debt and deficits. The Globe and Mail’s Jamie McGeever sums up debasement as “the fear that an oncoming inflationary storm could erode the dollar’s purchasing power and the value of U.S. financial assets[13]”. Some go further and forecast a U.S. dollar collapse.

It is true that the U.S. dollar has lost value recently relative to other major currencies, but this follows a period of dollar strength – a point recently made by the Globe and Mail’s Ian McGuggan: “Granted, the U.S. dollar has lost about 13 per cent of its value against a basket of other major currencies since 2022. But it’s hard to see how that justifies the 250-per-cent run-up in gold during the same period. The greenback is now trading roughly in line with its value from 2015 to 2020, when few people talked about dollar debasement[14].”

There are other problems with debasement theory, such as the conflicting signals being sent by the stock and bond markets. At present, these markets do not portend a crisis.

Writing in the Globe and Mail, Ian McGuggan explains: “If U.S. dollar debasement were an imminent threat, investors should be rushing to dump the greenback. U.S. bond yields should be soaring as investors seek extra compensation for the carnage that is to come. By and large, neither of these things is happening. U.S. bond yields are not doing much of anything. Meanwhile, people are still rushing to buy U.S. stocks, which are denominated in U.S. dollars.

The two trends represent diametrically opposed outlooks. The bull market on Wall Street suggests widespread euphoria about what lies ahead. The bull market in gold suggests a desperate search for safety[15]”.

A U.S. dollar crisis or imminent collapse is not very likely, but nevertheless there may be some substance to the debasement theory. The U.S. may very well choose to gradually allow the dollar to depreciate, as a means of reducing the real value of its debt. According to a recent FP article, this “soft default” strategy “is a well-worn playbook that has been used by heavily indebted states across history…. Soft defaults succeed because they avoid drama. No missed payments. No emergency summits. Just gradual erosion. For creditors, savers and allied economies, the message is clear. The risk is not nonpayment. The risk is repayment in diminished terms[16].

The U.S. dollar remains the world’s reserve currency (i.e. a foreign currency held in large quantities by central banks and monetary authorities to facilitate international trade, settle debts, and stabilize their own domestic currency), however some central banks have reduced U.S. dollar holdings replacing them with gold. According to Barron’s, “The U.S. dollar accounts for about 57% of central bank reserves, down from 64% in 2017.[17]” But Barron’s notes that “It’s more of a quiet diversification away from the dollar. Dollar diversification and dollar weakness shouldn’t be confused with de-dollarization[18].”

The debasement trade is a narrative that is, in some measure, fueling the recent bull market in gold and silver. It might be overstated. As Barron’s notes, “Even dollar bears aren’t calling for the end of the dollar’s reign as the world’s reserve currency. The dollar is still the most widely used currency—accounting for more than 90% of foreign exchange transactions—and the U.S. is the most liquid and deepest market. There’s no close competitor[19].”

The astute investor might heed Buffett’s warning that today’s investor must “hope people become more afraid in a year or two”. It is worth considering the possible downside when or if we reach peak “debasement trade”. Narratives, like stock market worries, tend to come and go.

Conclusion

- Gold and silver occasionally do outperform stocks and bonds, often during crises.

- Gold and silver can do well at times, but stocks win in the long run and by a large margin owing to compounding of earnings.

- Gold and silver are often seen as safe haven investments, but they can, in fact, be extremely volatile and buying into frenzies can be hazardous to your wealth, to borrow from Peter Lynch.

- Gold and silver prices have historically reached speculative peaks followed by severe corrections.

- Today’s buyer of gold and silver cannot determine an underlying or intrinsic value. Gold is tricky to value, as it doesn’t produce anything (unlike stocks that pay dividends that can grow over time). According to the FT: “… it’s just not clear what the fundamental value of gold is. It’s worth something because people have always thought it’s worth something”. In his 2011 Berkshire Hathaway shareholder letter, he described gold as having “two significant shortcomings, being neither of much use nor procreative[20].”

In Damodaran’s view, gold’s value is “driven largely by perception and market mood.” For this reason, prices can swing wildly owing to changes in sentiment.

- There is a possibility that the huge runup in prices over the past 12-18 months may be evidence of a bubble in the making.

Please note that we offer no prediction about the prices of gold and silver. Indeed, we believe that such forecasts cannot be reliably made by anyone. In writing this letter, we do not aim to dissuade or unnerve those of you who are enthusiastic about gold or silver as an investment. Rather, we wanted to provide you with our insights that you might find helpful and informative. In addition to growing and protecting your capital, we see this as an important part of our role in your investment journey. Thank you for allowing us to be your trusted advisors.

We hope that you have enjoyed this letter. Of course, please call us anytime to discuss further.

Best wishes to you and your family from your APEX team: Shawn, Mike, Denise N., Lisa, Connor, Marta, Jen, Denise E., John, Will, Jeannot, Andrene and Darlene.

Disclaimer:

This publication is for informational purposes only and has been prepared from public sources which are meant to be reliable. None of the information in this should be construed as investment advice. Speak to your Investment Advisor to learn if this product is right for you. Apex Investment Management is a tradename of Designed Securities Ltd. DSL is regulated by the Canadian Investment Regulatory Organization and a Member of the Canadian Investor Protection Fund Michael Begg and Shawn Malcolm are registered to advise in securities and/or mutual funds to clients residing in Ontario and B.C. The views expressed are those of the author and not necessarily those of DSL.

[1] McGeever, J. (2026, February 4). Record volatility is not what gold buyers signed up for. The Globe and Mail. https://www.theglobeandmail.com/investing/article-record-volatility-is-not-what-gold-buyers-signed-up-for/

[2] Bary, A. (2026, January 26). Silver Is Paying for Its Excesses. Silver Miner Stocks May Be a Buy. Barron’s. https://www.barrons.com/articles/silver-price-mining-stocks-683b3c2c?mod=Searchresults

[3] McGeever, J. (2026, February 4). Record volatility is not what gold buyers signed up for. The Globe and Mail. https://www.theglobeandmail.com/investing/article-record-volatility-is-not-what-gold-buyers-signed-up-for/

[4] Salisbury, I. (2026, January 2). 3 Signs Silver Prices May Be in a Bubble. Barron’s. https://www.barrons.com/articles/silver-gold-prices-bubble-bc1f720e

[5] Baccardax, M. (2026, January 26). Silver’s Parabolic Rally Sparks Bubble Warnings. Barron’s. https://www.barrons.com/articles/silver-parabolic-rally-bubble-fears-profit-taking-9e6d3edd

[6] McGeever, J. (2026b, February 4). Record volatility is not what gold buyers signed up for. The Globe and Mail. https://www.theglobeandmail.com/investing/article-record-volatility-is-not-what-gold-buyers-signed-up-for/

[7] Dauble, J. (2011, March 2). CNBC EXCERPTS: BILLIONAIRE INVESTOR WARREN BUFFETT ON CNBC’S “SQUAWK BOX” TODAY. CNBC. https://www.cnbc.com/2011/03/02/cnbc-excerpts-billionaire-investor-warren-buffett-on-cnbcs-squawk-box-today.html

[8] Gold in a Storm: How gold holds up during market crises | VanEck. (2025, May 27). Gold in a Storm: How Gold Holds up During Market Crises | VanEck. https://www.vaneck.com/us/en/blogs/gold-investing/gold-in-a-storm-how-gold-holds-up-during-market-crises/

[9] Damodaran, A. (n.d.). A golden year (2025): gold’s price surge – the signal in the noise! https://aswathdamodaran.blogspot.com/2025/11/a-golden-year-2025-golds-price-surge.html#:~:text=November%206%2C%202025-,A%20Golden%20Year%20(2025):%20Gold’s%20Price%20Surge%20%2D%20The%20Signal,ignore%20at%20their%20own%20peril

[10] Authers, J. (2010, October 22). Remember 1980: all that glitters is not gold. Mix of ideology and emotion can get in way of rationality. FT. https://www.ft.com/content/2919c20a-de09-11df-88cc-00144feabdc0

[11] ibid

[12] Authers, J. (2010, October 22). Remember 1980: all that glitters is not gold. Mix of ideology and emotion can get in way of rationality. FT. https://www.ft.com/content/2919c20a-de09-11df-88cc-00144feabdc0

[13] McGeever, J. (2025, October 20). Sorry gold bulls, but the ‘debasement trade’ theory doesn’t quite add up. The Globe and Mail. https://www.theglobeandmail.com/investing/article-roi-debasing-the-debasement-trade/

[14] McGugan, I. (2025b, October 20). Three reasons to be deeply skeptical about the current gold rally. The Globe and Mail. https://www.theglobeandmail.com/investing/markets/inside-the-market/article-gold-rally-skepticism-market-watchers/

[15] McGugan, I. (2025b, October 20). Three reasons to be deeply skeptical about the current gold rally. The Globe and Mail. https://www.theglobeandmail.com/investing/markets/inside-the-market/article-gold-rally-skepticism-market-watchers/

[16] Bryan Brulotte: America is quietly and softly defaulting on its debt. (2026, February 12). National Post. https://nationalpost.com/opinion/bryan-brulotte-america-is-quietly-and-softly-defaulting-on-its-debt

[17] Kapadia, R. (2026, February 19). The Reign of the Dollar Is Coming to an End. What Investors Can Do About It. Barron’s. https://www.barrons.com/articles/dollar-currencies-markets-investing-d823bedc

[18] ibid

[19] Kapadia, R. (2026, February 19). The Reign of the Dollar Is Coming to an End. What Investors Can Do About It. Barron’s. https://www.barrons.com/articles/dollar-currencies-markets-investing-d823bedc

[20] McKeever, V. (2020, April 20). Why people consider gold to be a “safe haven” in crises like the coronavirus. CNBC. https://www.cnbc.com/2020/04/20/coronavirus-why-gold-is-seen-as-a-safe-haven-investment-in-a-crisis.html